LP Secondaries

Allocation

DPI

"We're not short on opportunities. We're short on the hours to underwrite them properly. Every deal we pass on un-reviewed is a decision we made by not deciding."

We hear some version of this in nearly every conversation we have with LP-led secondary buyers. It is, by a wide margin, the number one thing teams tell us is holding them back. Not sourcing — the pipeline is full. Not capital — dry powder is at record levels (though only keeping pace with expected volumes). The binding constraint is the number of transactions a team of a fixed size can actually underwrite to a real answer before the bid date.

That constraint has tightened as the market has grown up. LP portfolios coming to market are larger and more diversified, often spanning dozens of underlying funds and hundreds of portfolio companies in a single line item. The work of forming a view on each one hasn't gotten faster. So the team becomes the bottleneck, and the bottleneck quietly sets the ceiling on how much the franchise can grow.

Here we want to lay out why that ceiling exists, and how the right operating model — built around a single, persistent forecast that is rolled forward each quarter rather than rebuilt each deal — lifts it.

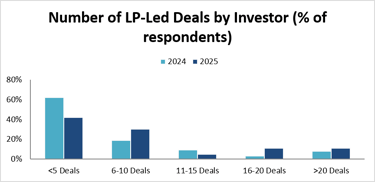

With both # of deals and average transaction size increasing...

Source: Lazard 2025 report

Source: Lazard 2025 report

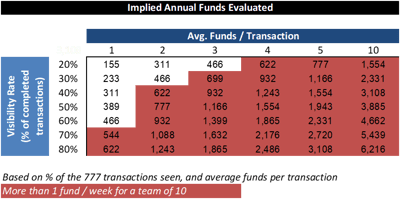

Investment teams are being asked to evaluate more funds on the same timeline...

Why LP-led underwriting struggles to scale

The reason a secondaries team can't simply review more deals is that the marginal deal is expensive to underwrite, and most of that expense is rebuilt from scratch every time.

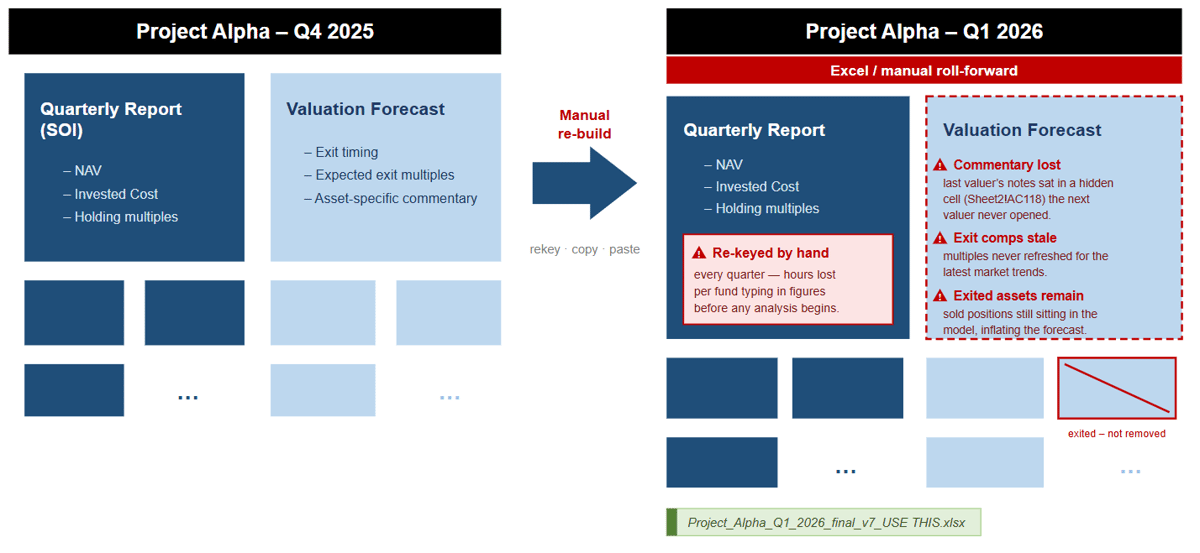

A typical LP-led underwriting cycle looks something like this. An analyst pulls the most recent capital account statements and quarterly reports for each underlying fund — often PDFs, often in different formats from different GPs. Cash flows get keyed into a model. A bottom-up or top-down forecast is built for each fund, layering in remaining value, expected distributions, and a pacing assumption. The fund-level forecasts are rolled up to a portfolio view, a discount rate or target return is applied, and a price emerges. Then the deal either closes or it doesn't — and either way, the model is filed away in a deal folder, frequently never to be opened again.

Three things make this slow, and all three compound as volume rises.

The work is duplicative. The same underlying funds show up across deal after deal. A team might underwrite the same flagship buyout fund a dozen times in a year for a dozen different LP portfolios, rebuilding a forecast each time because the prior work lives in a static spreadsheet inside someone else's deal folder. Institutional knowledge exists, but it isn't retrievable in a form the next deal can use.

The data work crowds out the judgment work. The hours that should go into the questions only a human can answer — is this GP's mark credible, is the pacing realistic, where is the tail risk — get consumed instead by extracting numbers from statements and reconciling them. The scarce resource is judgment and refining the forecast, and the manual process spends it on data entry.

Nothing persists. Because each deal produces a one-off artifact rather than updating a living view, the team's collective understanding of the funds it sees most often doesn't accumulate. The hundredth look at a manager starts roughly where the first one did.

The fix: one forecast, held and rolled forward

The alternative is to stop treating each deal as a blank page. Instead of a forecast that is born and dies inside a single transaction, the team maintains one forecast per underlying fund — a single, persistent object that is updated as new information arrives and re-used every time that fund appears in a new portfolio.

This is the idea at the center of how we've built Valumize. A few principles follow from it.

One forecast per fund, not one per deal. The unit of work becomes the fund, not the transaction. When a new LP portfolio comes in, the team isn't building forecasts — it's assembling a deal from forecasts it already maintains andnd building net-new only for the funds it hasn't seen before. The marginal deal gets dramatically cheaper, which is the entire point: cheaper marginal deals means more deals per analyst.

Rolled forward each quarter. When a new quarter's capital account statements and reports land, the forecast is rolled forward rather than rebuilt — actuals replace estimates, the remaining-value curve updates, and the prior assumptions are carried into the new period as a starting point to be revised, not re-derived. The quarter-end scramble becomes an update, not a reconstruction.

The forecast is the same object across every deal. Because there is one persistent forecast per fund rather than a scatter of deal-folder spreadsheets, a number means the same thing everywhere it appears. The pricing you ran in March and the re-underwrite you run in September sit on a continuous record, not two disconnected models that happen to share a fund name.

What this does to the data problem

Holding a persistent forecast only works if keeping it current is cheap. Two capabilities make that true:

Structured ingestion of GP reporting. Capital account statements and quarterly reports are pulled in and mapped to the right fund and period with the forecasts appended on top, so the quarterly roll-forward is a review step rather than a re-keying step. The numbers arrive where the forecast already lives.

A consistent treatment of marks and pacing. Because every fund's forecast is built on a common structure, assumptions are applied consistently across the portfolio rather than re-invented per analyst per deal — which is what makes the roll-up trustworthy and the senior review fast.

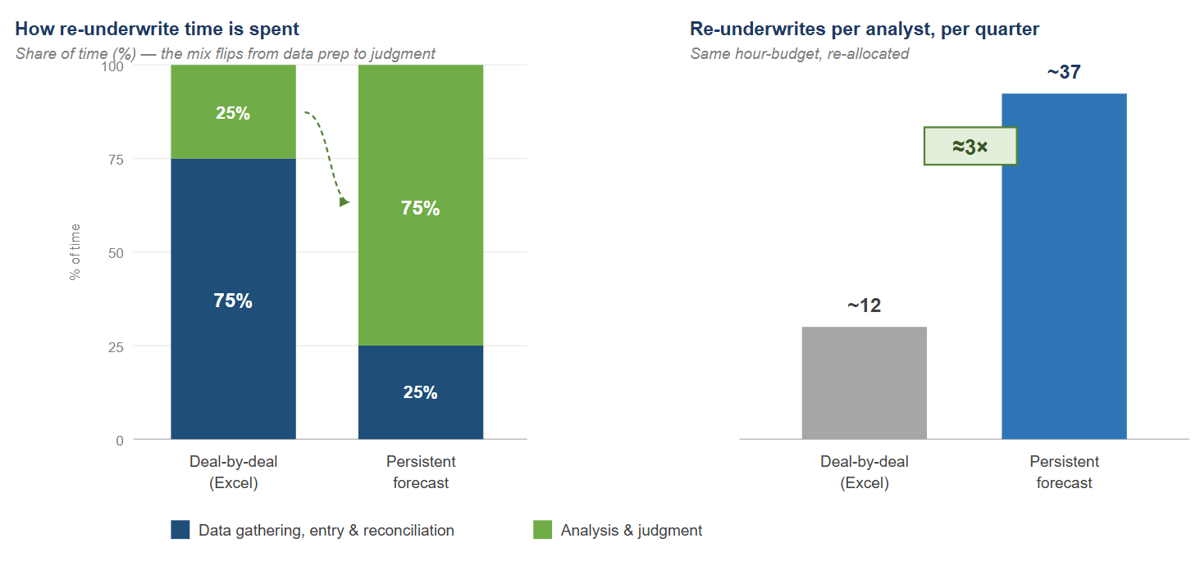

The effect is to flip where the team spends its hours. The data work shrinks toward a review-and-confirm step; the judgment work — the part that actually differentiates a buyer — gets the time back.

What changes when capacity is no longer the ceiling

When the marginal deal is cheap and the forecast persists, the throughput math changes in a few ways that matter to the franchise, not just the analyst.

More shots on goal. A team that can underwrite more portfolios to a real answer can bid on more, pass with conviction more often, and stop letting un-reviewed deals decide themselves. Win rate aside, simply being able to engage is the precondition for everything downstream.

Faster, more confident answers under a bid clock. Secondary processes run on tight timelines. A team starting from a maintained forecast of the funds in a portfolio is responding, not starting — which is the difference between a credible bid and a polite pass.

Knowledge that compounds. Each quarter's roll-forward makes the next deal involving those funds faster and better-informed. The franchise's understanding of the managers it sees most accumulates in one place instead of dissipating into deal folders.

Headcount that scales sub-linearly with volume. The promise isn't replacing judgment — it's that doubling deal volume shouldn't require doubling the team. The persistent forecast is the leverage point that breaks the one-analyst-per-N-deals relationship.

Source: Valumize internal analysis

The honest caveats

A persistent forecast is leverage, not magic, and it's worth being clear about what it doesn't do. It doesn't make a bad mark good — garbage in is still garbage out, and the quality of data (GP reporting, external data sources) remains the floor on what any model can know. It doesn't remove the need for senior judgment on the deals that matter; it redirects that judgment toward them. And rolling a forecast forward introduces its own discipline: assumptions carried from quarter to quarter have to be genuinely re-examined, not rubber-stamped, or yesterday's view quietly calcifies into today's blind spot. The operating model is built to make that re-examination easy — but it still has to happen.

The frame

The thing customers describe as a capacity problem is really an operating-model problem. A team that rebuilds every forecast from scratch has tied its growth to its headcount. A team that maintains one persistent forecast per fund and rolls it forward each quarter has not. That's the shift we built Valumize around, and it's why "we can finally look at more deals" is the line we most want to hear back.

In coming posts we'll get more concrete — how a fund-level forecast is actually constructed, how pacing and distribution assumptions layer across a fund's remaining life, and how a portfolio price falls out of the roll-up.